DePIN’s Revenue Dilemma: The Shaga Approach

DePIN networks proved that crypto incentives can bootstrap infrastructure at global scale. As the category evolves from infrastructure-first to revenue-first models, Shaga represents the next generation: architecting dual revenue streams (B2C gaming + B2B data licensing) for sustainable, demand-driven growth.

Key Points

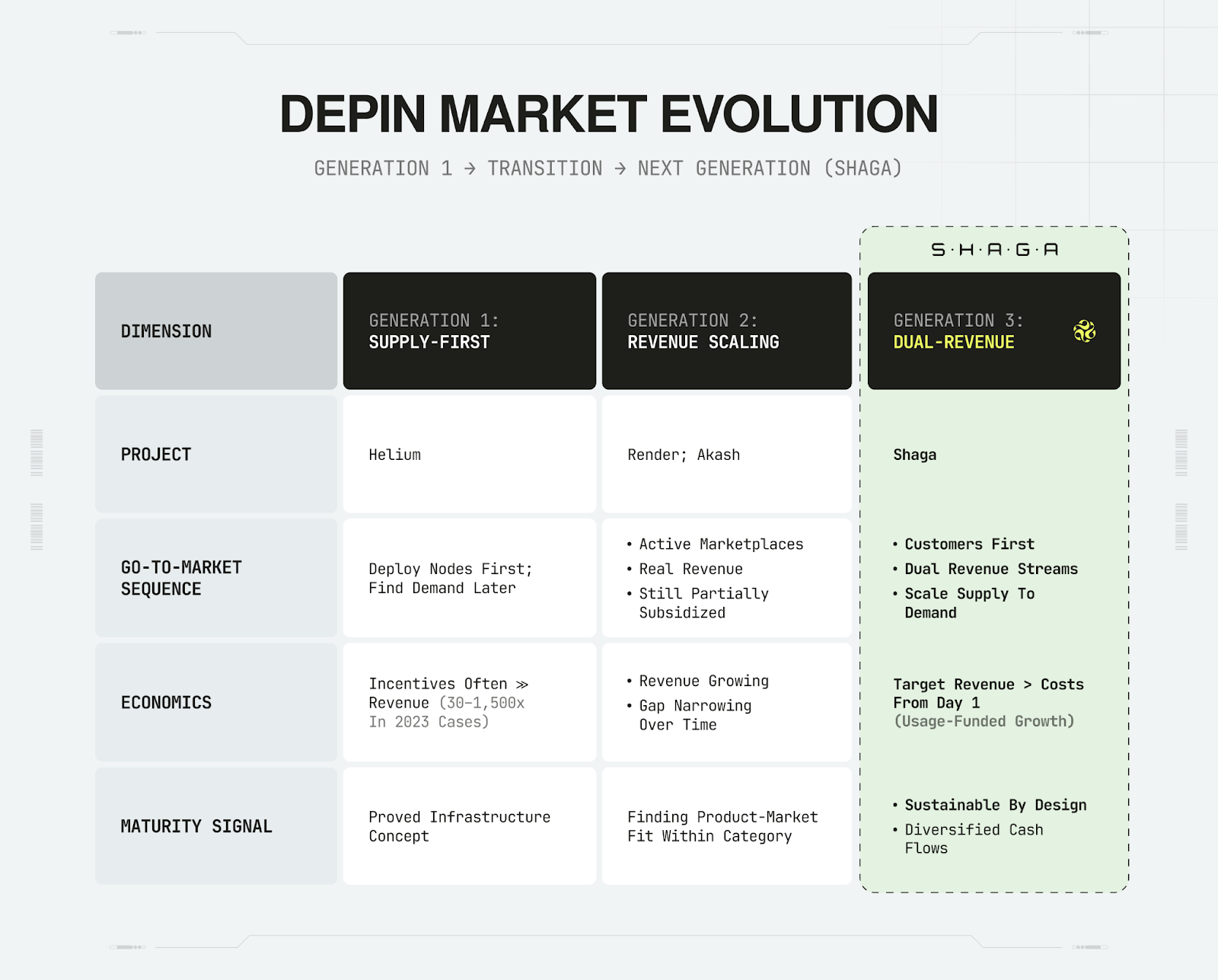

- DePIN pioneers successfully deployed large-scale infrastructure (Helium: 1M+ nodes), establishing the category foundation. The evolution toward revenue-first models represents the next phase of DePIN maturity.

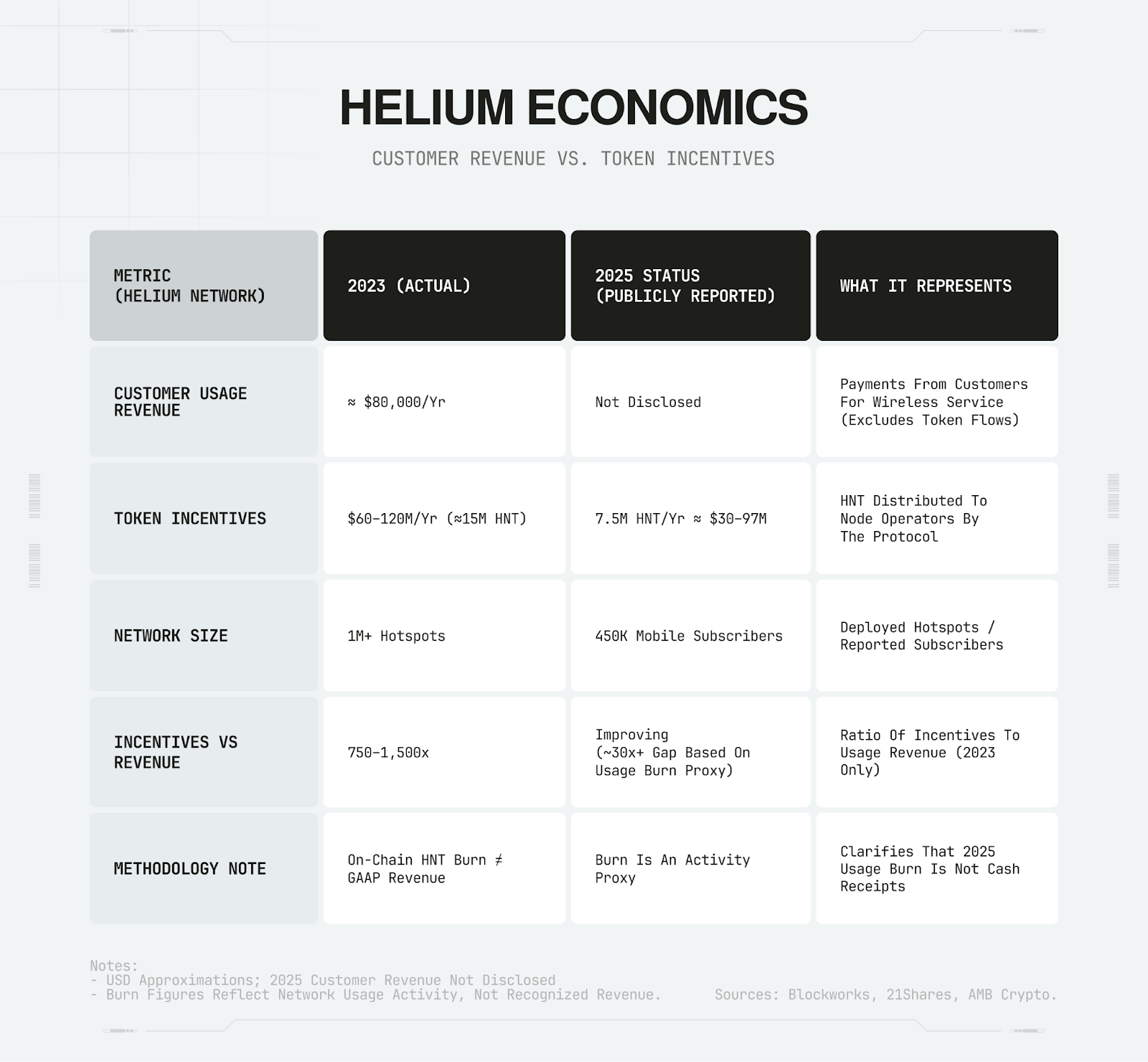

- Helium’s 2023 usage revenue was $6,651/month; 2025 shows $1M+ HNT burned from network usage (single data point, October 2025), while incentives total 7.5M HNT/year ($30-97M). Revenue ratio improved but still shows 30x+ disparity between incentives and customer usage.

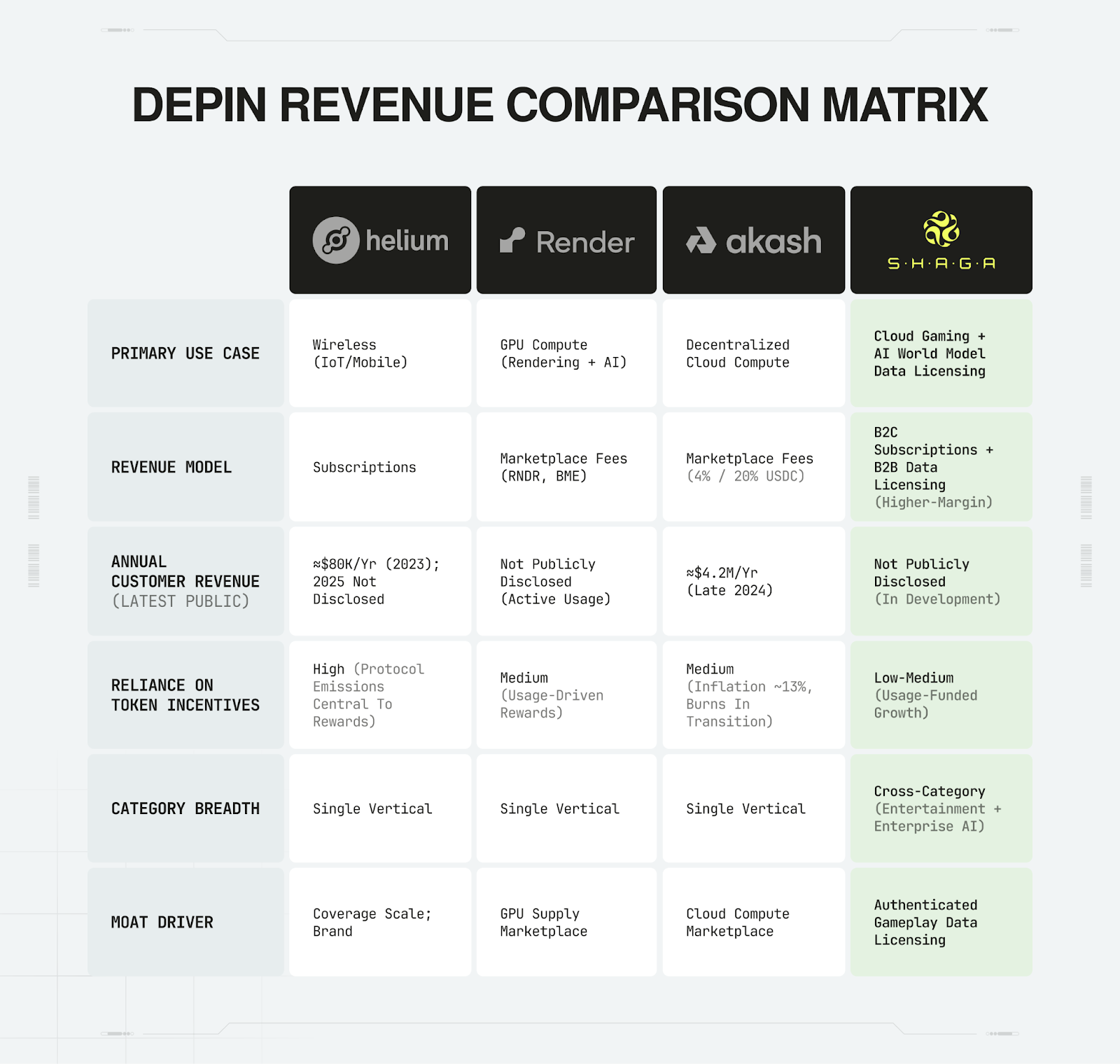

- Akash and Render demonstrate revenue generation ($4.2M/year revenue, active marketplaces), with Render serving both traditional rendering and AI workloads within the GPU compute category. Both show how DePIN infrastructure can serve paying customers.

- Shaga’s architectural approach combines consumer gaming infrastructure with AI data generation, designed to generate cash flow from distinct customer segments (entertainment + enterprise AI) while reducing dependence on token incentives for sustainable unit economics.

The DePIN sector’s pioneering success proved crypto can fund physical networks at unprecedented scale, establishing an entirely new infrastructure category.

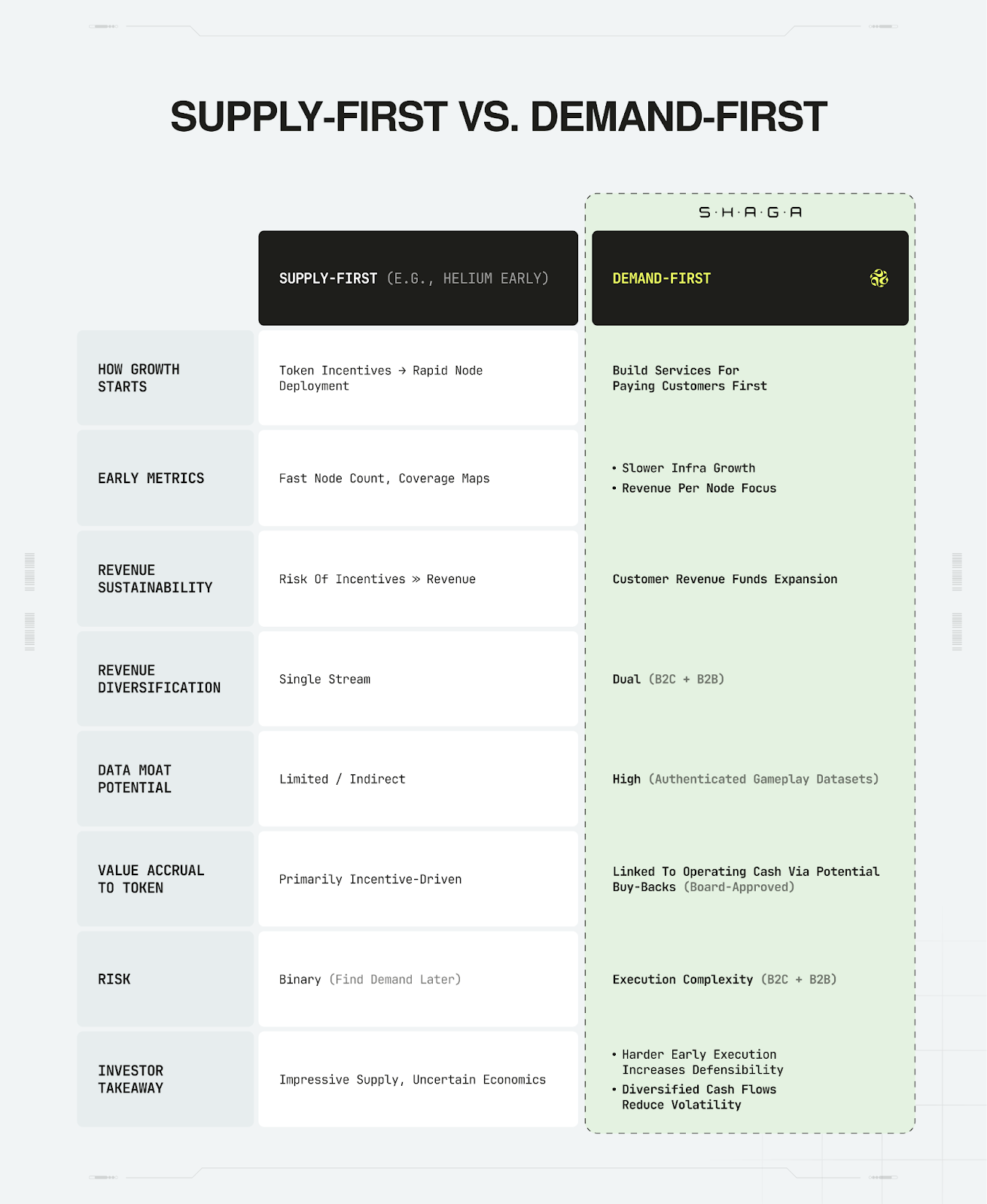

The early DePIN model prioritized network deployment to establish coverage and functionality. As the category matures, the evolution toward demand-first models that balance infrastructure growth with customer revenue represents the natural next phase.

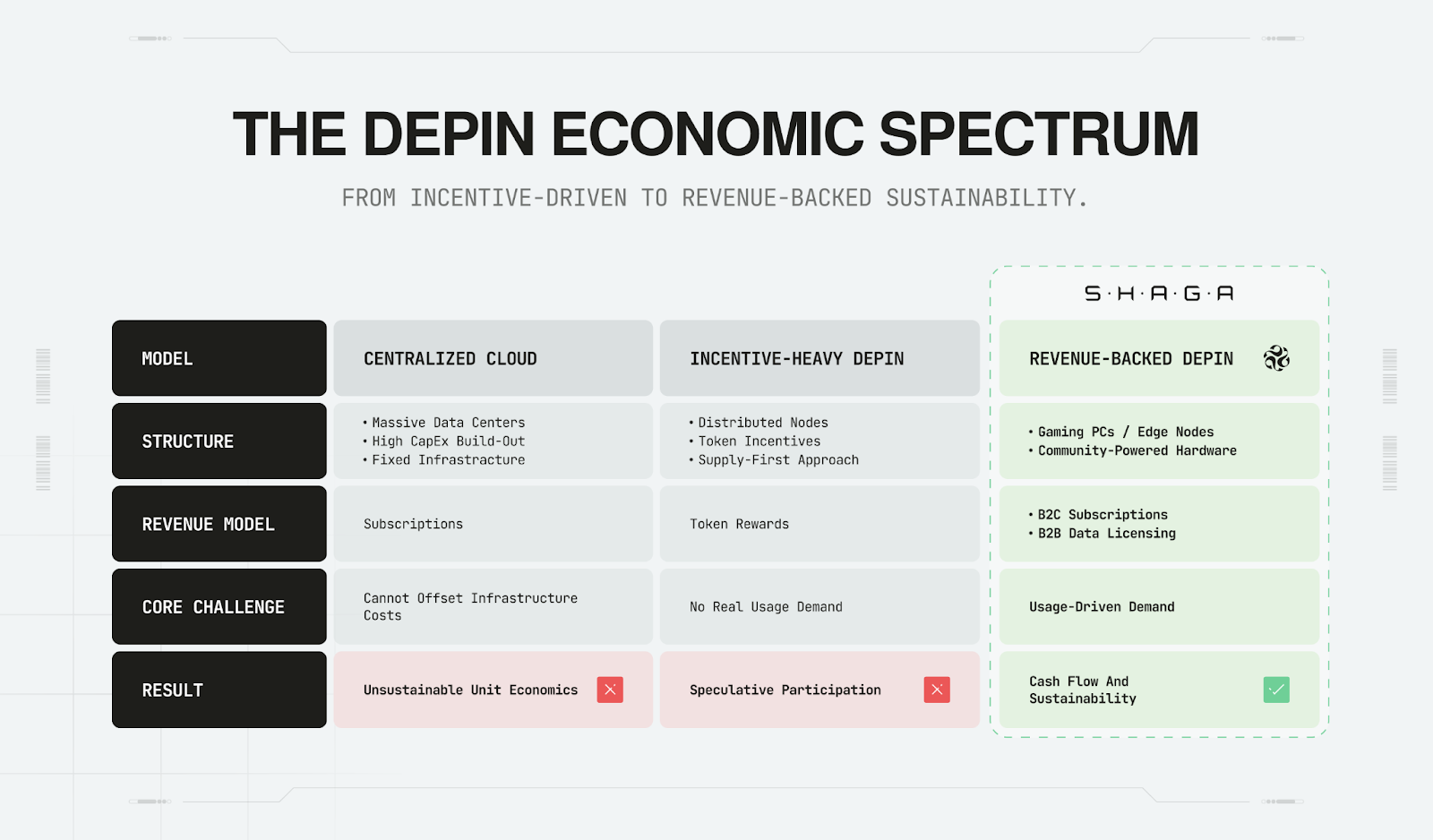

The DePIN playbook delivered remarkable infrastructure growth: Helium deployed over 1 million hotspots, Render built a GPU rendering marketplace, Akash created decentralized cloud infrastructure. These achievements proved crypto incentives can bootstrap physical networks at global scale. But infrastructure isn’t a business model. The question that defines DePIN sustainability isn’t how many nodes exist, it’s how much revenue comes from real paying customers.

For many DePIN networks, the answer shows a revenue/supply mismatch in parts of the sector.

The Helium Pioneer Model

Helium Network stands as the category-defining pioneer that proved DePIN could work. Their 1 million+ hotspots achieved what no centralized company could: global infrastructure bootstrapping through tokenized incentives at massive scale. This groundbreaking success established the foundation that the entire DePIN category builds upon today.

As with many pioneering models, Helium’s early phases prioritized network deployment over direct customer monetization. Blockworks analysis shows the network generated $6,651 from wireless network usage in June 2023, a baseline that reflects the infrastructure-first approach of category pioneers. The network has since evolved significantly, growing to 450,000 mobile subscribers as of September 2025. Recent activity shows $1M+ in HNT burned from network usage as a single data point from October 2025 (timeframe unclear from social media report), indicating substantial improvement in utilization. This evolution occurs alongside ongoing network incentives: 7.5 million HNT per year post-August 2025 halving, representing $30-97 million annually at current prices.

The shift becomes clear when comparing customer usage revenue vs token incentives:

Helium Network: Revenue vs. Incentive Evolution (2023–2025)

*Based on social media report; comprehensive revenue disclosures have not been published. Usage burn ≠ GAAP revenue; on-chain HNT burn is a proxy for network activity, not cash receipts. Additional context from secondary estimates: Solana DePIN sector revenue reported at varying levels across different sources (methodologies vary).

This data illustrates the characteristics of pioneering supply-first models: infrastructure deployment as the foundation for subsequent demand development.

Subsequent networks like Render and Akash began addressing this next phase, translating deployed infrastructure into sustained customer revenue.

Revenue-Generating Models: Render and Akash

Not all DePIN projects face Helium’s revenue gap. Render and Akash demonstrate that decentralized infrastructure can generate meaningful customer revenue when built around genuine market demand.

Render Network operates a GPU compute marketplace where creators and AI companies pay for distributed processing in RNDR tokens. The network serves both traditional 3D rendering (artists, studios, content creators) and AI workloads including training, inference, and generative imaging. The marketplace is active, with real customers purchasing real services across both segments. Render’s Burn-and-Mint Equilibrium (BME) model directs ~90-95% of network value to GPU operators, creating a sustainable loop where usage drives rewards. While Render serves multiple workload types, both operate within the broader GPU compute category.

Akash Network shows even stronger revenue traction, reaching $4.2 million annually in cloud compute revenue as of late 2024. Businesses lease decentralized cloud resources through Akash’s marketplace, generating actual usage revenue that significantly exceeds Helium’s customer payments. Akash’s model charges a 4% network fee on transactions (20% if paid in USDC), with portions burned to create deflationary pressure. Fees and burns reduce inflation over time, though revenue remains tied to one primary workload (cloud compute).

These networks prove that revenue-generating workloads exist in decentralized infrastructure. Each is experimenting with burn-and-mint models and deflationary mechanisms to reduce reliance on inflationary subsidies as usage scales. Akash’s documentation explicitly acknowledges this transition, describing the current ~13% inflation as “borrowing from the future” while marketplace demand catches up.

Both demonstrate that DePIN infrastructure can serve paying customers effectively. Render serves multiple workload types (traditional rendering + AI compute) within the GPU category, while Akash focuses on cloud compute infrastructure. Each has found market-fit for their infrastructure category and is evolving their tokenomics to optimize sustainability as usage scales.

Infrastructure Category Focus

Across the DePIN landscape, networks typically focus on one primary infrastructure category: Helium (wireless connectivity), Render (GPU compute for rendering and AI), Akash (cloud compute). Each successfully serves paying customers within its vertical.

The common characteristic: success depends on that infrastructure category scaling fast enough to support sustainable economics. Even when serving multiple workload types (like Render’s rendering + AI), the platform remains focused on a single infrastructure competency.

Where Shaga’s Model Differs

Shaga’s approach differs by crossing infrastructure categories: rather than focusing on one infrastructure vertical (wireless, GPU compute, cloud), Shaga combines consumer entertainment infrastructure with enterprise data generation.

As detailed in our analysis of Shaga’s dual-revenue model (see: “Dual Revenue, One Network: The Shaga Model”), the platform operates on community-powered edge computing where gaming PCs serve both consumer cloud gaming and enterprise AI data needs. Gamers access low-latency cloud gaming. When node operators opt in, the same sessions generate authenticated gameplay data for AI training, as explored in our examination of the AI training data market (see: “The AI Data Bottleneck”).

This approach is designed to create revenue diversification across different market categories: consumer entertainment subscriptions and enterprise AI data licensing. While networks like Render serve multiple workload types within GPU compute, Shaga crosses into different market verticals entirely—entertainment and enterprise AI—each with distinct customer bases, procurement cycles, and value propositions.

The architectural approach: Shaga is designed for demand-first scaling: attract paying customers (gamers + AI labs) with real value, then scale node supply to meet demonstrated demand. While Shaga remains in development with invite-only testing, this represents a different architectural approach compared to supply-first models that prioritize node deployment before customer validation.

This approach is more challenging to execute than supply-first models. It requires building consumer products people actually want and enterprise services customers will pay for, not just incentivizing hardware deployment. But this architectural difficulty, when executed successfully, creates differentiated unit economics. Building sustainable revenue from multiple paying customer bases requires different competencies than incentivizing supply expansion.

Why Revenue Architecture Determines Winners

The Helium experience highlights how early DePIN pioneers achieved what no centralized network could: global infrastructure bootstrapping through tokenized incentives. This supply-first model proved the concept—but also revealed the next stage of evolution for the category: aligning that scale with recurring, usage-driven revenue.

This shift marks the transition from first-generation infrastructure networks to sustainable, demand-first DePIN models. Sustainable DePIN evolution pairs incentive-driven growth with credible revenue streams from paying customers.

Render and Akash demonstrate that revenue-generating workloads exist in decentralized infrastructure. Their marketplace models prove customers will pay for decentralized GPU rendering and cloud compute. But both remain in the transition phase, where token economics and inflationary subsidies still support network growth while usage revenue scales.

Shaga’s cross-category approach positions the platform differently within DePIN. Rather than optimizing within one infrastructure vertical, the model combines consumer entertainment with enterprise AI data generation - different market categories with distinct customer economics. This architectural choice creates different unit economics and risk profiles compared to infrastructure-focused DePIN projects.

The competitive context includes established cloud gaming services with significant advantages: GeForce NOW benefits from NVIDIA’s brand and data center infrastructure, while Xbox Cloud Gaming leverages Microsoft’s enterprise relationships and Game Pass ecosystem. Traditional cloud gaming services typically don’t monetize gameplay data for AI training, creating an opportunity for purpose-built dual-use architectures.

Shaga’s differentiation lies in the dual-use architecture: the same gaming sessions that serve consumer demand also generate enterprise AI training data when node operators opt in. Because gameplay data licensing requires consent and provenance verification, Shaga’s node-operator opt-in and proof-of-origin systems are integrated into the capture pipeline from inception. This addresses specific friction points in current cloud gaming (limited data monetization, reliance on data center capital) while creating revenue streams that pure gaming services or pure AI data companies face barriers replicating through their existing architectures.

As DePIN Matures, Platforms That Pair Diversified Demand With Scalable Supply Will Define the Next Leaders

DePIN evolution shows a progression from infrastructure-first to revenue-first models. Pioneer networks like Helium proved the concept, while networks like Render and Akash demonstrate sustainable customer revenue within their infrastructure categories.

Shaga represents an architectural approach to this evolution: combining consumer entertainment infrastructure with enterprise AI data generation across different market verticals. This cross-category model is designed to create economic diversification through distinct customer segments (entertainment users + enterprise AI buyers) rather than optimizing within a single infrastructure category.

The execution challenge centers on successfully building consumer gaming demand while developing enterprise AI data capabilities that established gaming services and AI data companies can’t easily replicate through their existing architectures. This approach involves technical complexity (serving two distinct markets with different requirements), customer acquisition challenges across both consumer entertainment and enterprise AI segments, and regulatory considerations for AI data generation with proper consent frameworks. The architectural bet is that cross-category revenue diversification creates more durable unit economics than optimizing within single infrastructure categories.

As DePIN networks evolve from infrastructure to ecosystems, Shaga stands at the intersection, where gaming demand meets AI data supply, and growth compounds on both fronts.

Disclaimer: This analysis discusses DePIN infrastructure evolution, revenue models, and Shaga’s cross-category architectural approach - intended for informational and educational purposes, not for solicitation or investment promotion.